Trustees have a duty of loyalty – first and foremost to the beneficiaries of a trust. But what happens if a trustee steals from the trust, breaching their fiduciary duty? When a trustee acts in this fraudulent manner, they violate beneficiary rights and endanger trust assets. The abused beneficiaries can respond by petitioning for a trust accounting and then the eventual removal of the trustee.

While trust accountings can be an everyday occurrence in estate law, trustee fraud and embezzlement are just some of the startling discoveries that can be made. Fraudulently appropriating property that belongs to someone else, also known as embezzlement, is a serious crime. Law enforcement agencies can prosecute the theft of a property with a value of more than $950 as a felony, and civil wrongs arising from the same acts may be litigated in civil courts.

If you suspect that a trustee is committing fraud, the first step is to demand an accounting from the trustee. If they refuse to provide one, our highly experienced trust litigation attorneys will petition the probate court for a trust accounting.

If an accounting indicates that fraud or other malfeasance has occurred, we will counsel you about your options for having the trustee removed as well as bringing a lawsuit against them to recover trust assets that may have been lost. Call us at (916) 313-3030 for help.

The fiduciary relationship between the trust’s beneficiaries and the trustee is fundamentally built on the duty of the trustee to account. Trustees are required to keep accurate records that show trust income and disbursements and to provide this accounting to beneficiaries.

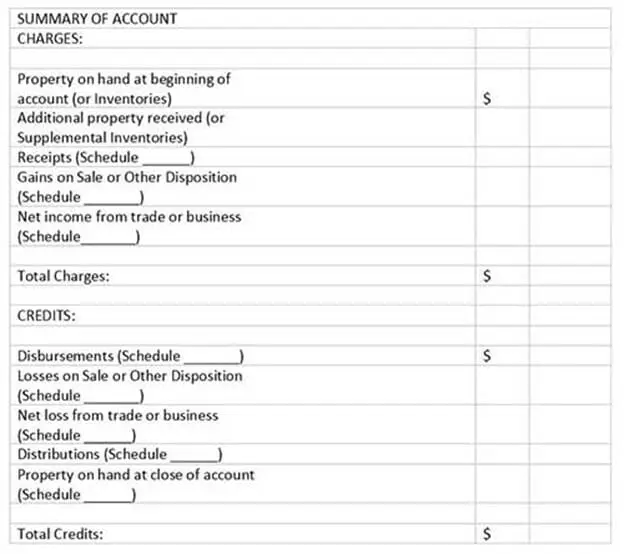

The duty to account is not optional: it can be enforced by a petition to the California Superior Court by a beneficiary having “exclusive jurisdiction of proceedings concerning the internal affairs of trusts.” Court accounting required schedules are found in California Probate Code § 1061.

This California statute provides:

Additional requirements for a court accounting are listed under California Probate Code § 1063. There is a mandate (among other requirements) in the statute that there be a “schedule of the estimated market value of the assets as of the beginning of the accounting period for all accounts subsequent to the initial account,” often the “weak link” for a trustee engaged in any wrongdoing.

Trustees who do not make an accounting are subject to legal action. In California, the three-year statute of limitations for trustee breach of duty becomes active only when the beneficiary receives a trustee accounting that “adequately discloses the existence of a claim against the trustee for breach of trust” or the beneficiary becomes aware of wrongdoing. If a trustee has committed wrongdoing, that liability can reach back decades.

Beneficiaries often employ trust and estate litigation counsel to sue trustees who choose to violate the duty to account. Laws requiring trustee accountings keep trustees from putting the assets of trust beneficiaries at risk. Whether the trustee is a trust company, bank, or individual, they must abide by these laws.

When trustees don’t abide by their duty to account, it could mean that wrongdoing is occurring and they are trying to hide it. What happens if a trustee steals or otherwise commits fraudulent acts? In addition to potential criminal charges, beneficiaries can make them pay for their actions in civil court.

Our skilled trust and estate litigation lawyers stand up for beneficiaries who are being defrauded by unscrupulous trustees. Call us at (916) 313-3030 if a trustee is refusing to account and you believe they may be stealing from a trust or otherwise committing fraudulent acts against the trust.

When a trustee does not provide an accounting, the odds skyrocket that there has been a breach of fiduciary duty. Violating the rule exposes beneficiaries to partial or complete loss of assets that a deceased parent or relative wanted them to have. There are several different ways that a trustee may breach their fiduciary duty. Some are more intentional than others, but any of them can expose beneficiaries to losses.

Examples of breach of fiduciary duty by a trustee are:

To discover whether breaches have occurred, forensic accountants are called in to do careful line-by-line examinations of trust records. Any breaches uncovered during this trust accounting will most likely provide cause for removal of the trustee. A trustee is called upon to be honest and loyal in administering a trust. If they breach their fiduciary obligations to beneficiaries, the beneficiaries have every right to petition for trust accounting and removal of the bad trustee.

Our trust litigation attorneys at Hackard Law represent abused beneficiaries who, because of trustee inaction or refusal, must file a petition to the probate court for a trust accounting. Any petition for a trust accounting in a California Superior Court must follow the specific rules of the probate code. We understand the specific rules a petition must follow and can assist you with your petition. We can be reached at (916) 313-3030.

Once the trustee has made an accounting, the beneficiary and their attorneys will closely examine all documents. Should the trustee fail to keep accurate records, they are presumed to have violated their fiduciary duties. Even if a trustee has failed to keep accurate records simply because they don’t have the required organizational skills to manage a trust, they can be subject to removal. When they intentionally defraud a trust, they may be held accountable in both criminal and civil courts, depending on the circumstances. We can advise you about recourse in your case.

Here are some real life and unfortunate examples of breach of fiduciary duty that involve individual trustees:

Illinois certified public accountant, Sultan Issa, was charged with criminal fraud for allegedly embezzling at least $55 million from a Chicago family and its related business entities, including trusts established for charitable giving and to provide for the large family. The case is currently pending in federal court in Illinois.

Longtime Connecticut trusts and estates attorney, Robert J. Barry, pleaded guilty to one count of wire fraud relating to his theft from elderly client trust accounts. Barry would often designate himself as successor trustee in trusts that he prepared for clients. He also had himself named as executor of his client’s estate upon death.

The Department of Justice press release described his scheme: “Beginning at least as early as 2008 and continuing until approximately December 2015, BARRY engaged in a scheme to defraud an elderly victim by stealing money from the victim’s client trust accounts while the victim was alive, and then stealing money from the victim’s estate after the victim died… Through this scheme, BARRY stole more than $2.4 million from the victim and the victim’s estate.”

Michigan financial advisor, David Homan, was charged with felony embezzlement charges for allegedly stealing more than $500,000 from a trust fund where he was the appointed trustee for two elderly clients. An independent audit of the trust fund showed significant electronic transfers of money from the fund to Mr. Homan’s personal bank accounts. Homan pleaded guilty in November 2018 to one felony count of embezzlement between $50,000 and $100,000. He sentenced was two to 15 years in prison and ordered to pay restitution in the amount he stole – $513,211.56.

Tennessee attorney, Jackie Lynn Garton, was charged with wire fraud, aggravated identity theft, and tax fraud related to a years-long scheme where Garton, acting as a trustee, stole over $350,000 from the trust of a minor whose father, a Tennessee State Trooper, was killed in the line of duty. The beneficiary, Carina Larkins, was told by Garton that her money was growing. When she learned it was a lie she said, “Shock is an understatement, I was absolutely devastated, I couldn’t breathe.” Garton pleaded guilty to stealing over $1.36 million from trust funds of clients, including Carina Larkins. He was sentenced to 92 months in jail.

Ohio caregiver, Teresita Sidoti, pleaded guilty to bank fraud and filing false tax returns related to her embezzlement of $156,949.75 between 2009 and 2015 from a trust established by the victim’s parents to pay the medical expenses for an Ohio resident, Noel Zugay, who was totally disabled with multiple sclerosis. The U.S. Attorney’s office handling the case said that Sidoti worked as Zugay’s caregiver and controlled bank accounts for Zugay and the trust. She took the money by writing checks to herself, transferring money online and by making withdrawals in person. Sidoti was sentenced to 2 ½ years in federal prison for defrauding the trust.

California caregiver, Donna Crick, pleaded guilty to a single charge of theft or embezzlement from a 92-year-old-man suffering from dementia. “Once Crick had drained the life savings from the victim’s bank accounts (about $172,000), Crick convinced the victim to make Crick the trustee and beneficiary of the victim’s living trust, his home, his annuity and his life insurance,” according to a (Kern County) District Attorney’s office release.

A 58-year-old Michigan man was sentenced to 23 months to five years in prison for embezzling over $20,000 from his 93-year-old mother. Family members contacted law enforcement when they became concerned that the man was siphoning money from his mother. This initiated a Michigan State Police criminal investigation and charges were brought against the son.

Ricky Bradford Willson, holder of a durable power of attorney for his 90-year-old great aunt, “transferred $120,000 in cash from his aunt’s bank account into his, signed a quit claim deed transferring her house in …(Michigan) to himself, and transferred the title of her classic 1967 Ford Mustang convertible to himself.” Attorney General Dana Nessel called this “a classic example of financial elder abuse: a trusted relative who took advantage of his aunt.”

So, it’s likely that all of the families and beneficiaries defrauded by these schemes would share the same emotions as Carina Larkins, the Tennessee beneficiary:

“Shock is an understatement, I was absolutely devastated, I couldn’t breathe.”

There is a very good reason that California and other states impose a duty on trustees to keep clear and accurate accounts. When trustees fail to keep proper accounts, they can be held accountable in court.

Hackard Law represents aggrieved beneficiaries in estate, trust, probate and elder financial abuse civil matters. We take serious cases where we think that we can make a substantial difference and there is a wrongdoer who can be made financially accountable for their wrongdoing or breach of duty.

We represent foreign, out-of-state and California clients in California trust and estate litigation. We focus our geographic reach to California’s largest urban areas, including Los Angeles, Orange, Santa Clara, San Mateo, Alameda, Contra Costa and Sacramento Counties.

If you would like to speak with us about your case, call our experienced attorneys at (916) 313-3030.

(916) 313-3030

(916) 313-3030